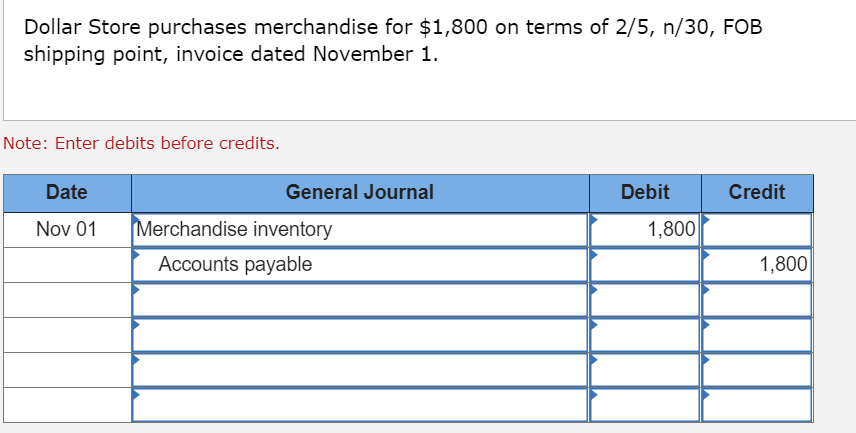

- You might eradicate your residence for those who get behind into the financing costs.

- In the event that assets viewpoints decline, your own shared first mortgage and you will home equity mortgage you’ll set you upside-down, definition your debt over you reside value.

Professionals

- You’ve got the option to pay just appeal during the mark period; this could mean your monthly installments be in check than the the newest repaired payments towards a house security financing.

- You don’t need to fool around with (and you can pay back) all of the financing you have been acknowledged to have. Focus is billed entirely on the amount you borrowed.

- Certain HELOCs come with a transformation option which enables you to place a fixed price towards particular otherwise all equilibrium. This may let shield your allowance away from changing-price increases.

Downsides

- HELOCs have changeable pricing. Inside the a surfacing-interest rate environment, it means you’ll spend a great deal more month-to-month. It unpredictability can become tough on the finances.

- Of a lot HELOCs incorporate a yearly fee, and several include prepayment punishment, aka cancellation or very early cancellation charge, if you shell out the line of prior to when the fresh repayment plan determines. Domestic equity lenders have a tendency to ask you for to own varying-to-fixed-rates sales, also.

- You can get rid of your home in order to property foreclosure if not pay the brand new line of credit.

- In the event the property philosophy decline instantly or a depression happens, the lending company you are going to lower your credit line, frost they if not request quick payment completely.

HELOCs in which he Finance have blossomed within the prominence in recent times. True, originations of domestic guarantee money have been off 8 percent 12 months over year (out of Q4 2022 to Q4 2023) based on TransUnion’s newest Household Security Styles Declaration, in addition to their HELOC cousins elizabeth several months. However, which lag is somewhat deceivingpared to help you before many years, house equity originations are very well above the rates filed on last half dozen years.

What’s the appeal? From mid-2022, the latest RIIR (an upswing during the rates) – for example mortgage pricing, which have doubled since their middle-pandemic lows – have decimated the newest beauty of dollars-aside refinancing, since wade-to answer to tap an effective homeownership share. Hence, the interest home based guarantee money and HELOCs. When you find yourself these types of products’ prices features risen nowadays too – HELOCs in particular ended 2023 more than ten percent – they’ve stabilized and also decrease inside the 2024. Trying to the long run, HELOC prices is projected in order to decline even further, possibly averaging regarding 8.45 per cent towards the end of this 12 months.

Naturally, this household-equity borrowing is established you are able to because of the number-function escalation in home values as the start of pandemic, that has increased the value of homeowners’ security bet. The typical mortgage holder presently has $206,000 within the tappable guarantee, up out of $185,000 last year, predicated on Freeze Financial Tech, a bona fide house analysis investigation company.

How can you explore household guarantee?

Each other family guarantee funds and you may HELOCs allows you to make use of the finance you discover fit. Of several consumers use them to pay for significant home repairs otherwise home improvements, including completing a basements, remodeling a kitchen or updating your bathroom. Anybody else utilize them to settle large-desire personal credit card debt, initiate a click for info corporate otherwise defense college can cost you.

Therefore, how much money would you use which have property equity mortgage or HELOC? Sometimes, dramatically. Loan providers tend to place minimums out of $10,000 with the devices, and you may maximums is also encounter half a dozen rates.

The exact number you might borrow, whether or not, is determined by several facts, together with your guarantee stake while the restriction security fee that the bank allow you to acquire. Your mortgage balance plus performs a task, since your bank usually means your current domestic-obligations weight to remain lower than a certain part of the house’s well worth.